How to pay off $50,000 in debt in 1 year?

Facing a $50,000 debt can feel overwhelming, but paying it off within a year is achievable with a strategic plan. This article outlines a practical roadmap to aggressively tackle your debt, incorporating proven strategies like the debt snowball and avalanche methods. We'll explore budgeting techniques, identifying areas for significant savings, and negotiating with creditors to potentially lower interest rates. Learn how to create a realistic repayment schedule, stay motivated, and finally break free from the burden of significant debt in just 12 months. Let's get started!

Aggressive Strategies for Eliminating $50,000 in Debt Within 12 Months

Create a Realistic Budget and Track Your Spending

Paying off $50,000 in a year requires extreme discipline and a meticulously crafted budget. Start by listing all your income sources and meticulously tracking every expense. Utilize budgeting apps or spreadsheets to gain a clear picture of your financial situation. Identify areas where you can drastically cut back – this might mean reducing dining out, entertainment, subscriptions, or even temporarily downsizing your living situation. The key is to maximize your savings and direct every extra dollar towards debt repayment. The more accurately you track your spending, the better you can allocate funds effectively and stay on track with your aggressive repayment plan. Remember, consistency is crucial; regularly reviewing and adjusting your budget will ensure you remain accountable and adapt to any unexpected changes in your income or expenses.

Explore Debt Consolidation and Balance Transfer Options

Consider consolidating your high-interest debts into a lower-interest loan or utilizing a balance transfer credit card with a 0% introductory APR period. This strategy can significantly reduce the amount you pay in interest over the year, freeing up more funds to apply directly to the principal balance. Carefully compare offers from different lenders or credit card companies to find the best terms and fees. Remember to calculate the total cost, including any transfer fees or penalties, to ensure it aligns with your repayment goal. Time management is critical here; you need to act swiftly to secure the best options before the introductory periods expire, thereby maintaining the lower interest rate as long as possible. However, be mindful that consolidating debt isn't always the most suitable solution for everyone; it’s essential to carefully weigh the pros and cons and ensure you can make the required minimum payments consistently.

Increase Your Income Through Additional Work or Side Hustles

Paying off a significant amount of debt in a short timeframe often requires boosting your income. Explore opportunities to increase your earnings, such as taking on a part-time job, freelancing, or starting a side hustle aligned with your skills and interests. Even small increases in income can make a considerable difference when directed towards debt repayment. Be creative in finding extra income streams – consider selling unused items, renting out a spare room, or offering services like tutoring, pet sitting, or house cleaning. Commitment is key; you need to consistently dedicate additional time and effort to generate this supplemental income. The more income you can generate, the faster you'll reach your goal of becoming debt-free in a year. Remember to factor in any additional expenses associated with these activities when budgeting your extra income.

This content may interest you! How do I get out of owing money?

How do I get out of owing money?| Strategy | Pros | Cons |

|---|---|---|

| Budgeting & Tracking | Improved financial awareness, increased control over spending | Requires discipline and consistent effort |

| Debt Consolidation/Balance Transfer | Lower interest rates, simplified payments | Potential fees, risk of accumulating more debt if not managed carefully |

| Increased Income | Faster debt repayment, improved financial stability | Requires extra time and effort, potential for burnout |

How long will it take to pay off $50,000 in debt?

Paying Off $50,000 in Debt

The time it takes to pay off $50,000 in debt depends entirely on several key factors. There's no single answer. The most significant factors are your monthly payment amount and the interest rate on your debt. A higher monthly payment will obviously reduce the payoff time, while a lower interest rate will also significantly shorten the repayment period. Other factors include whether you're making extra payments, whether you consolidate your debt, and the type of debt (credit cards typically have higher interest rates than loans).

Interest Rate's Impact

The interest rate dramatically affects how long it takes to pay off your debt. A higher interest rate means more of your monthly payment goes towards interest, leaving less to pay down the principal balance. This slows down the repayment process. Conversely, a lower interest rate allows a larger portion of your payment to reduce the principal, accelerating repayment. Consider the following examples (assuming a fixed monthly payment):

This content may interest you! How do I clear my bank debt?

How do I clear my bank debt?- High Interest Rate (e.g., 20% on credit cards): The payoff period could extend for many years, even with substantial monthly payments.

- Moderate Interest Rate (e.g., 8% on a personal loan): The payoff period would be significantly shorter compared to a high-interest rate.

- Low Interest Rate (e.g., 3% on a debt consolidation loan): This will result in the fastest repayment time.

Monthly Payment Amount

The amount you pay monthly is directly proportional to the repayment time. Larger monthly payments reduce the time it takes to pay off the debt, while smaller payments extend the repayment period. It's crucial to find a balance between an affordable monthly payment and a reasonable repayment timeline. Factors to consider include your income, expenses, and other financial obligations.

- High Monthly Payment: Results in a shorter repayment period, but requires a higher level of disposable income.

- Moderate Monthly Payment: Offers a balance between affordability and a manageable repayment timeline.

- Low Monthly Payment: Stretches the repayment period over a longer time, potentially accumulating more interest.

Debt Consolidation and Extra Payments

Debt consolidation and making extra payments are effective strategies to accelerate debt repayment. Consolidating high-interest debts into a single loan with a lower interest rate can significantly reduce the overall interest paid and shorten the repayment timeline. Making extra payments, even small ones, can substantially decrease the time it takes to become debt-free. This is because the extra payments reduce the principal faster, leading to less interest accruing in the long run.

- Debt Consolidation: Streamlines payments and may lower the interest rate, leading to faster repayment.

- Extra Payments: Any additional amount paid beyond the minimum payment directly reduces the principal, shortening the repayment period.

- Snowball or Avalanche Method: These methods prioritize payments to either the smallest debt first (snowball) or the highest interest debt first (avalanche) to create a sense of accomplishment and efficiency.

Is 50k in debt a lot?

Is 50k in Debt a Lot?

This content may interest you! Is $20,000 a lot of debt?

Is $20,000 a lot of debt?Whether $50,000 in debt is a lot depends entirely on your individual circumstances. There's no single answer. It's relative to your income, the type of debt, and your overall financial situation. A $50,000 student loan for a high-earning profession might be manageable, while the same amount in high-interest credit card debt could be crippling. Consider your debt-to-income ratio (DTI), which compares your monthly debt payments to your gross monthly income. A high DTI indicates a greater financial burden. Also, the interest rates on your debt are crucial; high-interest debt compounds quickly, making it harder to pay off. Ultimately, assessing whether $50,000 is "a lot" requires a thorough evaluation of your personal financial health.

Factors Determining if $50,000 in Debt is Significant

Several key factors influence whether a $50,000 debt is manageable or overwhelming. Your income plays a crucial role; a higher income allows for larger monthly payments, making debt repayment more feasible. The type of debt also matters – low-interest student loans are generally easier to manage than high-interest credit card debt. Finally, your overall financial situation, including assets and savings, contributes to the overall picture. Having substantial assets can offset the impact of the debt, while a lack of savings exacerbates the problem.

- Income: High earners can often manage $50,000 in debt more easily than lower earners. Your ability to make consistent, substantial payments directly impacts the speed of repayment and the overall stress associated with the debt.

- Debt Type: Student loans, mortgages, and auto loans usually have lower interest rates than credit cards. This difference directly affects the total amount paid over time and the monthly payment burden.

- Financial Assets: Existing savings and investments can buffer the impact of high debt. These assets can serve as a safety net or be used to pay down the debt more quickly.

Strategies for Managing $50,000 in Debt

If $50,000 in debt feels overwhelming, several strategies can help manage it. Creating a detailed budget to track income and expenses is crucial for identifying areas to cut back. Prioritizing high-interest debt using methods like the debt avalanche (paying off highest interest first) or debt snowball (paying off smallest debt first) can significantly reduce the total interest paid over time. Consolidating debt into a single loan with a lower interest rate can simplify payments and potentially reduce the total cost. Seeking professional financial advice from a credit counselor or financial advisor can provide personalized guidance and support.

- Budgeting: A thorough budget helps identify areas for spending reductions, freeing up funds for debt repayment. This is crucial for managing any debt, and more so when dealing with a significant amount.

- Debt Reduction Strategies: Employing methods like the debt avalanche or snowball allows for a strategic approach to debt repayment, focusing on either minimizing interest or achieving quick wins.

- Debt Consolidation: Consolidating multiple debts into one loan can simplify repayment and potentially lower the overall interest rate.

The Importance of Seeking Professional Advice

Managing a significant debt like $50,000 can be challenging, and seeking professional guidance is highly recommended. A financial advisor can assess your individual circumstances, create a personalized debt repayment plan, and offer advice on improving your financial health. Credit counseling agencies can provide support and resources for managing debt, including debt management plans. They can also negotiate with creditors to lower interest rates or monthly payments. Remember that seeking help is not a sign of failure, but rather a proactive step towards financial well-being.

This content may interest you! What to do if you are in massive debt?

What to do if you are in massive debt?- Financial Advisors: Provide personalized financial plans tailored to individual needs, offering expert guidance on managing debt and improving financial stability.

- Credit Counseling Agencies: Offer support and resources for managing debt, including debt management plans and negotiation with creditors.

- Debt Management Plans (DMPs): Structured plans managed by credit counseling agencies that consolidate debt, often with lower interest rates and monthly payments.

How to pay off a $50,000 loan fast?

Paying Off a $50,000 Loan Fast

How to Pay Off a $50,000 Loan Fast?

Paying off a $50,000 loan quickly requires a dedicated and strategic approach. There's no magic bullet, but combining several effective methods can significantly reduce the repayment time and overall interest paid. The key is to increase your payments as much as possible while minimizing expenses and maximizing income.

Increase Your Payments

The most direct way to pay off your loan faster is to increase your monthly payments. Even a small increase can make a substantial difference over time due to the power of compounding interest. Consider exploring different payment options with your lender, such as making bi-weekly payments instead of monthly. This effectively adds an extra monthly payment each year. Alternatively, you can make lump-sum payments whenever you have extra funds available, such as tax refunds, bonuses, or unexpected windfalls.

This content may interest you! What to do when you are heavily in debt?

What to do when you are heavily in debt?- Calculate the impact of increased monthly payments using an online loan amortization calculator.

- Explore the possibility of bi-weekly payments with your lender.

- Identify potential sources of extra funds for lump-sum payments (bonuses, tax returns, side hustles).

Reduce Expenses and Increase Income

To free up more money for loan repayment, focus on both reducing unnecessary expenses and increasing your income streams. Carefully review your monthly budget, identifying areas where you can cut back. This may involve reducing dining out, entertainment, subscriptions, or other discretionary spending. Simultaneously, explore ways to boost your income, such as taking on a side job, freelancing, or selling unused possessions.

- Create a detailed budget to track your income and expenses.

- Identify areas where you can reduce spending (e.g., subscriptions, entertainment).

- Explore opportunities to increase your income (e.g., part-time job, freelance work).

Refinance Your Loan

Refinancing your loan can potentially lower your interest rate, reducing the overall cost and allowing you to pay off the debt faster. Shop around for lenders offering competitive rates and terms. Be aware of any refinancing fees, and ensure the overall savings outweigh these costs. Consider refinancing to a shorter loan term, even if the monthly payments are slightly higher, as this will significantly decrease the total interest paid over the life of the loan.

- Compare interest rates and terms offered by different lenders.

- Carefully consider the total cost, including any refinancing fees.

- Evaluate the potential benefits of a shorter loan term.

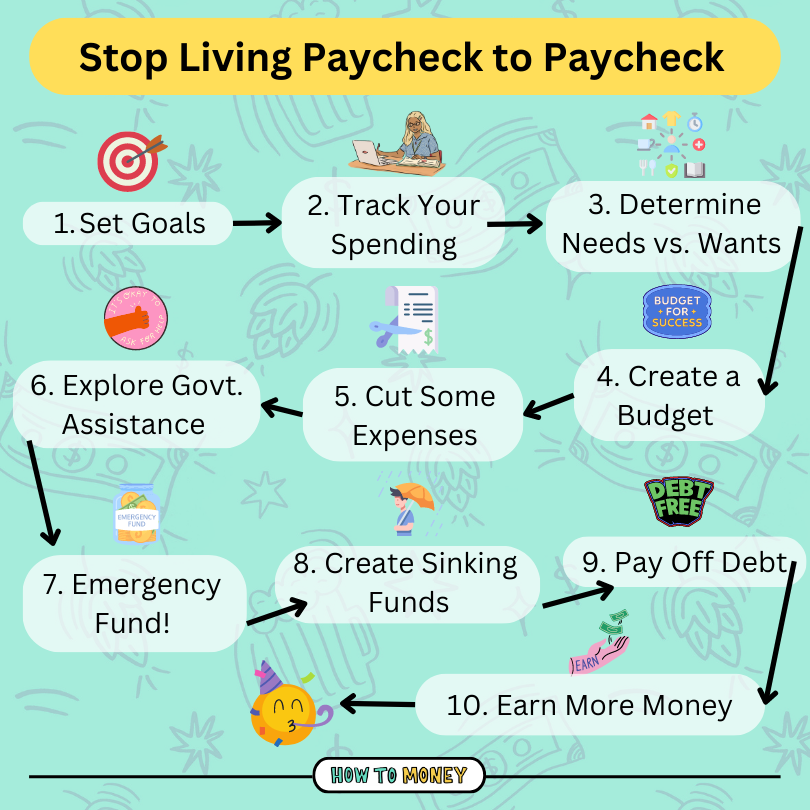

How do I pay off debt if I live paycheck to paycheck?

Paying Off Debt While Living Paycheck to Paycheck

This content may interest you! How to consolidate debt and lower interest rates?

How to consolidate debt and lower interest rates?Paying off debt while living paycheck to paycheck is challenging, but achievable with careful planning and discipline. The key is to create a budget that prioritizes debt repayment while still covering essential expenses. This requires a multi-pronged approach focusing on increasing income, reducing expenses, and strategically allocating your resources. You'll need to be realistic about your financial situation and patient, as it's a process that takes time and effort. There's no magic solution, but consistent effort will yield results.

Create a Realistic Budget

The foundation of debt repayment is a meticulously crafted budget. This involves tracking every dollar coming in and going out. Use budgeting apps, spreadsheets, or even a notebook to monitor your spending habits. Once you have a clear picture of your income and expenses, you can identify areas for potential savings and allocate funds towards debt reduction. Prioritize essential expenses (housing, food, utilities, transportation) and cut back on non-essentials. This clear picture will show exactly where your money goes, allowing for more informed decisions.

- Track every expense for at least a month to get a clear picture of your spending habits.

- Categorize your expenses (housing, food, transportation, entertainment, etc.) to identify areas for potential savings.

- Create a realistic budget that allocates funds for debt repayment while covering essential expenses.

Explore Ways to Increase Your Income

While reducing expenses is crucial, increasing income provides more resources to tackle your debt. Explore various avenues to boost your earnings. This could involve seeking a higher-paying job, taking on a part-time job or freelance work, selling unused possessions, or renting out a spare room. Every extra dollar contributes to faster debt repayment. Don't underestimate the power of small, additional income streams. Even a small increase can make a big difference over time.

- Look for higher-paying jobs in your field or consider a career change.

- Explore freelance opportunities or part-time jobs to supplement your income.

- Sell unused items online or through consignment shops to generate extra cash.

Develop a Debt Repayment Strategy

Once you have a budget in place and have potentially increased your income, it's time to strategize your debt repayment. Popular methods include the debt snowball (paying off the smallest debt first for motivational wins) and the debt avalanche (paying off the debt with the highest interest rate first for financial efficiency). Choose the strategy that best suits your personality and financial situation. Remember to stay consistent and avoid accumulating new debt. Consider consolidating high-interest debt into a lower-interest loan if available.

This content may interest you! How can I save money if I have debt?

How can I save money if I have debt?- Choose a debt repayment method (snowball or avalanche) and stick to it.

- Automate your debt payments to ensure consistency.

- Avoid accumulating new debt while paying off existing debts.

Is it even possible to pay off $50,000 in debt in one year?

While challenging, it's possible with aggressive strategies and significant lifestyle changes. Success hinges on a high income relative to your debt, a strong commitment to eliminating expenses, and potentially multiple income streams. You'll need a detailed budget, prioritizing debt payments over all other spending except for essential living costs. Consider debt consolidation to simplify payments and possibly secure a lower interest rate. The key is dedication and meticulous financial planning.

What's the best debt repayment strategy for this goal?

The avalanche method focuses on paying off the highest-interest debts first, minimizing overall interest paid. Alternatively, the snowball method tackles the smallest debts first for motivational wins, boosting momentum. Both require discipline. Consider a combination: prioritize the highest-interest debt, but make small payments on others for psychological encouragement. Regularly review your progress and make adjustments as needed, remaining adaptable to unexpected events.

How can I increase my income to accelerate repayment?

Explore all avenues for increasing your income. This could include a second job, freelancing, selling unused possessions, or taking on a side hustle. Consider negotiating a salary increase at your current job. If you have valuable skills, offer them as a service. Be creative and resourceful; any extra income significantly impacts your ability to repay the debt quickly. Remember to factor in the time commitment of any additional income source to ensure its practicality.

What lifestyle changes are necessary to achieve this?

Significant lifestyle adjustments are crucial. Analyze your spending meticulously, cutting unnecessary expenses. Reduce dining out, entertainment costs, and subscriptions. Prioritize needs over wants. Consider cheaper housing options if feasible. Explore free or low-cost recreational activities. The goal is to maximize the portion of your income dedicated to debt repayment. This period of financial austerity is temporary; the long-term reward is freedom from debt.

Leave a Reply