How does income tax work?

Understanding income tax can feel daunting, but it's a crucial aspect of financial literacy. This article breaks down the complexities of how income tax works, from determining your taxable income to understanding different tax brackets and filing your return.

We'll cover deductions, credits, and common pitfalls to help you navigate the system effectively and ensure you're paying the correct amount. Whether you're a first-time filer or seeking to optimize your tax strategy, this guide offers clear explanations and practical advice.

Understanding the Basics of Income Tax

Income tax is a direct tax levied on an individual's or entity's earnings. The fundamental principle is that the government collects a portion of your income to fund public services like infrastructure, education, and healthcare.

The amount you owe depends on several factors, including your total income, taxable deductions, and the applicable tax brackets. Different countries have their own specific tax systems, with varying rates and rules.

However, the core concept remains the same: individuals and businesses contribute a percentage of their earnings to support government operations. It's crucial to understand your tax obligations to ensure compliance and avoid penalties.

Taxable Income and Deductions

Your taxable income isn't simply your gross income. It's the amount left after subtracting allowable deductions. These deductions can significantly reduce your taxable income and, consequently, your tax liability.

Common deductions often include contributions to retirement accounts (like 401(k)s or IRAs), mortgage interest payments (in some countries), charitable donations, and certain business expenses (for self-employed individuals).

Accurately calculating your deductions is vital for minimizing your tax burden. It is important to consult with a tax professional or utilize tax software to ensure you are claiming all eligible deductions.

This content may interest you! What is the difference between tax deductions and tax credits?

What is the difference between tax deductions and tax credits?Tax Brackets and Progressive Taxation

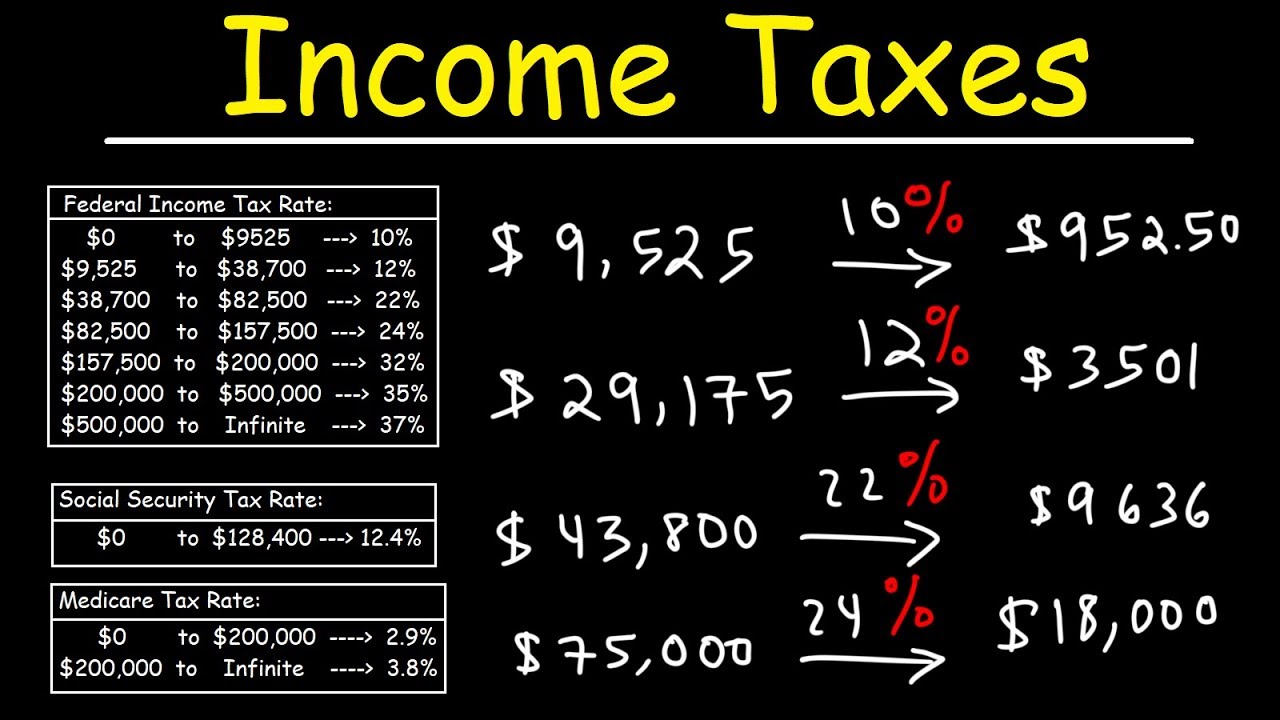

Most income tax systems employ a progressive tax structure. This means that the tax rate increases as your income rises. Your taxable income is categorized into different tax brackets, each with its own tax rate.

You don't pay the highest rate on your entire income; instead, you pay the applicable rate for each portion of your income that falls within a specific bracket.

For example, you might pay 10% on the first $10,000, 15% on the next $20,000, and so on. This system ensures that higher earners contribute a larger percentage of their income in taxes, promoting a more equitable distribution of the tax burden.

Filing Your Tax Return

Filing your tax return is the process of officially reporting your income and calculating your tax liability to the relevant tax authority. This usually involves completing a tax form and submitting it by a specific deadline.

Accurate and timely filing is crucial to avoid penalties and interest charges. The specific requirements vary depending on your location and tax situation. You may choose to file your return yourself, utilize tax preparation software, or seek assistance from a tax professional.

Gathering all necessary documentation, including W-2s, 1099s, and receipts for deductions, is a key step in preparing your return.

| Term | Definition |

|---|---|

| Gross Income | Your total income before deductions. |

| Taxable Income | Your income after deductions, which is subject to taxation. |

| Tax Brackets | Income ranges with associated tax rates. |

| Tax Deductions | Allowable subtractions from gross income that reduce taxable income. |

| Tax Credits | Direct reductions in the amount of tax owed. |

| Tax Return | The form used to report income and calculate tax liability. |

How do income taxes actually work?

Income taxes are a system where governments levy taxes on the income earned by individuals and businesses.

The process varies significantly by country, but the core principles remain similar. Generally, it begins with the calculation of taxable income, which involves subtracting allowable deductions and exemptions from gross income.

This content may interest you! How do tax brackets work?

How do tax brackets work?The resulting taxable income is then subjected to tax rates, which are often progressive, meaning higher earners pay a larger percentage of their income in taxes. The tax liability is calculated based on these rates, and the taxpayer is responsible for paying this amount to the relevant tax authority, usually through a system of withholding (taxes deducted from paychecks) and annual filing of a tax return.

Failure to pay taxes or underpayment can result in penalties and interest. The specific rules, rates, and deductions are established by laws and regulations that are subject to change.

Determining Taxable Income

Determining your taxable income is the first crucial step in the process. This involves calculating your gross income – the total amount of money earned from various sources such as wages, salaries, investments, and business profits.

From this gross income, you then subtract various deductions and exemptions that are allowed under the tax law. These can range from standard deductions (a fixed amount) to itemized deductions (specific expenses like charitable donations or mortgage interest), depending on the tax system and individual circumstances.

The result is your adjusted gross income (AGI), which is then further adjusted based on other factors to arrive at your taxable income. The accuracy of this calculation is paramount to avoiding tax-related issues.

- Gather all income documentation (W-2s, 1099s, etc.)

- Identify and calculate eligible deductions (standard or itemized).

- Accurately complete the relevant tax forms to determine AGI and taxable income.

Applying Tax Rates and Calculating Tax Liability

Once taxable income is determined, the next step is calculating your tax liability. This involves applying the relevant tax brackets or rates to your income. Most tax systems employ a progressive tax structure, where different income levels are taxed at different rates.

Lower income brackets typically face lower tax rates, while higher income brackets face higher rates. The tax liability is computed by applying the appropriate rate to each portion of your income that falls within a specific bracket.

This results in the total tax owed. This calculation can be complex, especially for high-income earners or those with intricate financial situations. Tax software or professional tax preparation services can be incredibly helpful in this step.

This content may interest you! What is a tax refund and how can I get one?

What is a tax refund and how can I get one?- Consult the applicable tax brackets for your tax year and filing status.

- Apply the correct rates to each portion of your taxable income within each bracket.

- Sum the taxes from each bracket to arrive at your total tax liability.

Tax Filing and Payment

The final stage involves filing your tax return and paying your taxes. Taxpayers typically have a deadline to file their returns, which details their income, deductions, and calculated tax liability. This return is submitted to the relevant tax authority.

Throughout the year, most taxpayers have taxes withheld from their paychecks (through payroll withholding) or make estimated tax payments. This helps ensure that taxes are paid regularly.

After filing, the tax authority reviews the return, and if the taxes withheld or paid are less than the calculated liability, the taxpayer owes the difference. Conversely, if more was paid, a refund may be issued. Accurate record-keeping and timely filing are vital to avoid penalties and interest.

- Gather all necessary documents and complete the relevant tax forms.

- File the return by the designated deadline.

- Pay any outstanding taxes owed or claim a refund.

How are income taxes calculated?

Income tax calculation varies significantly depending on the country and its specific tax laws. However, the general process involves several key steps. First, you determine your gross income, which is your total income from all sources before any deductions.

This includes wages, salaries, interest, dividends, capital gains, and other forms of income. Next, you subtract allowable deductions and exemptions. These can include things like contributions to retirement accounts, certain medical expenses, charitable donations, and dependent care expenses.

The result is your taxable income. Then, your taxable income is applied to a tax bracket system, where different income levels are taxed at different rates. The tax owed is calculated based on the applicable rate for each bracket of your income.

Finally, any tax credits you qualify for are subtracted from your calculated tax liability to arrive at your final tax bill (or refund if you overpaid). The specific deductions, exemptions, brackets, and credits available depend entirely on the tax laws of the relevant jurisdiction.

This content may interest you! How can I legally reduce my taxes?

How can I legally reduce my taxes?Determining Gross Income

Gross income is the foundation of the tax calculation. It encompasses all forms of income received during the tax year. Accurately reporting your gross income is crucial for a correct tax computation. Failure to do so can result in penalties.

- Wages and salaries from employment

- Interest income from savings accounts and bonds

- Dividends from investments in stocks

- Capital gains from the sale of assets

- Rental income from properties

- Self-employment income

Applying Tax Brackets and Rates

Most tax systems use a progressive tax structure, meaning higher income levels are taxed at higher rates. Tax brackets define income ranges, each associated with a specific tax rate.

The calculation involves determining which bracket(s) your taxable income falls into and applying the corresponding rates to the portions of income within each bracket. The final tax liability is the sum of the tax amounts for each bracket.

- Each tax bracket has a defined income range.

- Each bracket is associated with a specific tax rate.

- Taxable income is allocated to each applicable bracket.

- The tax for each bracket is calculated separately.

- The total tax liability is the sum of the taxes from all brackets.

Tax Credits and Deductions

Tax credits and deductions reduce your tax liability. Credits directly reduce the amount of tax you owe, while deductions reduce your taxable income. Understanding the difference is crucial for minimizing your tax burden.

Many tax credits and deductions are available, depending on individual circumstances. It is important to claim all eligible credits and deductions to accurately calculate the tax due.

- Tax credits directly lower the tax owed.

- Deductions reduce taxable income, lowering the tax rate applied.

- Eligibility for credits and deductions varies depending on factors like income, family status, and expenses.

- Claiming all eligible credits and deductions is essential for accurate tax calculation.

- Documentation is necessary to support the claims for credits and deductions.

How does income tax work for dummies?

Income tax is a tax levied on your earnings. Governments use this revenue to fund public services like schools, roads, and healthcare. The amount you owe depends on your taxable income – that's your gross income (total earnings) minus certain deductions and allowances.

The tax system uses a progressive structure, meaning higher earners pay a larger percentage of their income in taxes than lower earners. This is usually achieved through tax brackets.

This content may interest you! What expenses can I deduct from my taxes?

What expenses can I deduct from my taxes?Each bracket has a different tax rate, and your income is taxed at the rate corresponding to each bracket it falls into. For example, the first portion of your income might be taxed at 10%, the next portion at 15%, and so on. You won't pay the highest bracket's rate on your entire income; only the portion that falls within that bracket.

What are Tax Brackets?

Tax brackets are ranges of income that are taxed at specific rates. The government sets these rates, and they can change annually. Your total tax liability is calculated by adding up the tax owed from each bracket your income falls into.

It's important to note that tax brackets are marginal, not average. This means you only pay the higher rate on the income within that specific bracket, not your entire income.

- Each bracket has a minimum and maximum income level.

- The tax rate associated with each bracket increases as income increases.

- You only pay the higher rate on the portion of your income that falls within the higher bracket.

What are Deductions and Allowances?

Deductions and allowances reduce your taxable income, lowering the amount of tax you owe. Deductions are expenses you can subtract from your gross income, while allowances are fixed amounts that can be subtracted.

Common deductions include charitable contributions, certain business expenses, and mortgage interest (depending on location and specific rules). Allowances might include those for dependents or certain retirement contributions.

The availability and specifics of deductions and allowances vary depending on your location and tax laws.

- Deductions directly reduce your taxable income.

- Allowances provide a set amount reduction to your taxable income.

- Properly claiming deductions and allowances is crucial for minimizing your tax liability.

Filing Your Taxes

Tax filing is the process of submitting your tax return to the relevant tax authority. This return summarizes your income, deductions, and tax calculations. Many countries have specific deadlines for filing, and failure to file on time can result in penalties.

You can file your taxes yourself using tax software or online portals, or you can hire a tax professional to assist you. Keeping accurate records of your income and expenses throughout the year is vital for a smooth filing process.

This content may interest you! What are the different types of taxes?

What are the different types of taxes?- Gather all necessary tax documents (W-2s, 1099s, etc.).

- Choose a filing method (software, online portal, tax professional).

- File your return by the deadline to avoid penalties.

What is my tax bracket if I make $60,000?

Determining your exact tax bracket at $60,000 requires knowing your filing status (single, married filing jointly, head of household, etc.) and whether you have any deductions or credits. The US tax system is progressive, meaning higher incomes are taxed at higher rates.

However, you only pay the higher rate on the portion of your income that falls into that bracket, not your entire income. To find your exact bracket, you need to consult the official IRS tax brackets for the relevant tax year.

These brackets are updated annually. Sites like the IRS website or tax software programs will provide the most up-to-date and accurate information.

Taxable Income vs. Gross Income

Your gross income is your total income before any deductions. Your taxable income, on the other hand, is the amount of your income that is actually subject to taxation after accounting for deductions and adjustments.

For example, contributions to a 401(k) or IRA can reduce your taxable income. The tax bracket you fall into depends on your taxable income, not your gross income.

- Gross income represents your total earnings from all sources, including wages, salary, self-employment income, interest, dividends, and capital gains.

- Taxable income is calculated by subtracting allowable deductions and adjustments from your gross income. These deductions and adjustments are based on various factors, including your filing status and eligible expenses.

- Understanding the difference is crucial for accurate tax calculations. Using your gross income to estimate your tax bracket will likely provide an inaccurate result.

The Importance of Filing Status

Your filing status significantly impacts your tax bracket. The IRS offers several filing statuses, each with its own set of tax brackets. Filing as "single" will generally result in a higher tax burden than filing jointly with a spouse.

Other statuses like "head of household" or "qualifying widow(er)" provide different tax advantages. Choosing the correct filing status is essential for accurate tax calculations.

- Single: For unmarried individuals.

- Married Filing Jointly: For married couples who combine their incomes and deductions.

- Married Filing Separately: For married couples who file separate returns.

- Head of Household: For unmarried individuals who maintain a home for a qualifying child or dependent.

- Qualifying Surviving Spouse: For a surviving spouse who meets specific criteria.

State Taxes and Local Taxes

Federal income tax is just one component of your overall tax liability. Many states also have income taxes, and some localities impose additional taxes. These state and local taxes can significantly impact your overall tax burden.

This content may interest you! What are taxes and how do they work?

What are taxes and how do they work?The tax rates vary substantially among states and localities. To determine your total tax liability, you must calculate your federal tax, your state tax, and any local taxes.

- State income tax rates differ widely, with some states having no income tax at all.

- Local taxes, such as city or county income taxes, can further increase your overall tax obligation.

- It's important to understand both your federal and state/local tax obligations to accurately determine your total tax liability.

What is income tax?

Income tax is a direct tax levied on individuals or entities' earnings. The amount of tax owed depends on the taxable income, which is calculated after deducting allowable expenses and deductions. Tax rates are typically progressive, meaning higher earners pay a larger percentage of their income in taxes.

The revenue generated from income tax is a crucial source of funding for government services, such as healthcare, education, and infrastructure projects. Tax laws and regulations vary significantly between countries, influencing the specifics of calculation and the applicable rates.

How is my taxable income calculated?

Your taxable income is determined by subtracting allowable deductions and exemptions from your gross income. Gross income encompasses all sources of income, including salaries, wages, investment returns, and business profits.

Allowable deductions might include contributions to retirement plans, mortgage interest payments, charitable donations, and certain business expenses. Exemptions can reduce taxable income further, often based on factors like marital status or number of dependents.

The specific deductions and exemptions vary by jurisdiction and tax laws, so consulting tax resources specific to your location is crucial for accurate calculation.

What are the different types of income tax systems?

Several income tax systems exist globally. Progressive systems, common in many developed countries, impose higher tax rates on higher income brackets. Regressive systems, less common, levy a higher percentage on lower incomes.

Proportional systems apply a flat tax rate across all income levels. Some countries employ a combination of these, incorporating features from multiple systems. Understanding your country's system is vital for accurate tax preparation.

This content may interest you! How can I file my taxes correctly?

How can I file my taxes correctly?Consult with a tax professional for guidance on navigating complex aspects of your specific system.

What happens if I don't pay my income tax on time?

Failing to pay income tax on time can lead to significant penalties and interest charges. The severity of the consequences varies depending on the jurisdiction and the extent of the delay.

Penalties can include late payment fees, added interest on the unpaid amount, and potentially even legal action in cases of significant non-compliance. Furthermore, a poor tax history can impact credit scores and future borrowing capabilities.

To avoid these issues, diligent tax planning and timely filing are essential. If facing difficulties, seeking professional tax advice is recommended to explore available options and mitigation strategies.

Leave a Reply