How do tax brackets work?

Understanding tax brackets is crucial for effective financial planning. This article demystifies the often-confusing system of progressive taxation. We'll explore how tax brackets are structured, clarifying the marginal tax rate and its impact on your overall tax liability. Learn how your income falls into different brackets, determining the percentage of tax you owe on each portion. We'll also address common misconceptions and offer practical examples to help you navigate this vital aspect of personal finance. By the end, you'll have a solid grasp of how tax brackets work and how they affect your bottom line.

How Tax Brackets Determine Your Tax Liability

Tax brackets are a system used by many countries to calculate income tax. They don't mean that all of your income is taxed at the highest rate you fall into. Instead, they work on a marginal basis. This means that each dollar you earn is taxed at the rate corresponding to the tax bracket it falls into. Only the portion of your income that falls within a specific bracket is taxed at that bracket's rate. The lower brackets are taxed at lower rates, creating a progressive tax system where higher earners pay a larger percentage of their income in taxes. Let's say you have a tax system with brackets of 10%, 20%, and 30%. If your income is $50,000 and the brackets are structured so that the first $20,000 is taxed at 10%, the next $20,000 at 20%, and anything above that at 30%, only the portion of your income in each bracket will be taxed at that specific rate. It's not a case of paying 30% on your entire income.

Understanding Marginal Tax Rates

The marginal tax rate is the tax rate applied to the last dollar you earn. It's crucial to understand that this doesn't mean your entire income is taxed at this rate. For example, if your marginal tax rate is 25%, it only means that the money you earn above a certain threshold is taxed at 25%. Income earned below that threshold will still be taxed at the lower rates corresponding to the relevant brackets. Therefore, your average tax rate (the overall percentage of your income paid in taxes) will typically be lower than your marginal tax rate.

The Importance of Tax Deductions and Credits

Tax deductions and tax credits can significantly reduce your overall tax liability. Deductions lower your taxable income, effectively shifting your income to a lower tax bracket or reducing the amount taxed at higher rates. Credits, on the other hand, directly reduce the amount of tax you owe. For example, a $1,000 tax credit directly reduces your tax bill by $1,000, regardless of your tax bracket. Both deductions and credits are valuable tools for lowering your tax burden and are often dependent on various factors, such as income level, family size, and eligible expenses. Understanding these can greatly affect how much you ultimately pay in taxes.

This content may interest you! What is a tax refund and how can I get one?

What is a tax refund and how can I get one?How Tax Brackets Change Over Time

Tax brackets aren't static; they can be adjusted periodically by governments. These adjustments often reflect changes in inflation, economic conditions, and policy decisions. Inflation adjustments can prevent "bracket creep," where inflation pushes taxpayers into higher brackets without a real increase in purchasing power. However, governments may also actively change tax bracket thresholds and rates to achieve specific fiscal policy goals, like stimulating the economy or reducing the national debt. It's vital to stay informed about changes to tax laws and brackets to ensure accurate tax calculations.

| Income Range | Tax Rate |

|---|---|

| $0 - $10,000 | 10% |

| $10,001 - $40,000 | 15% |

| $40,001 - $80,000 | 25% |

| $80,001+ | 30% |

How do tax brackets actually work?

How Tax Brackets Work

How Do Tax Brackets Actually Work?

Tax brackets are a system used by many governments to calculate income tax. Instead of applying a single tax rate to all income, a progressive system uses different rates for different income levels. Each range of income is called a tax bracket, and each bracket has its own tax rate. Your total taxable income isn't taxed at the highest rate you fall into; rather, only the portion of your income within each bracket is taxed at that bracket's rate. This means that the higher your income, the higher the average tax rate you will pay, but not necessarily a proportionally higher marginal rate.

This content may interest you! How can I legally reduce my taxes?

How can I legally reduce my taxes?How Marginal Tax Rates Work

The tax rate applied to each bracket is called a marginal tax rate. This is the rate applied only to the income within that specific bracket. It's important to understand that your marginal tax rate is not the rate you pay on all of your income. For example, if you earn $50,000 and the brackets are structured so that the first $10,000 is taxed at 10%, the next $20,000 at 15%, and the remaining at 20%, your income is not taxed at 20% across the board. Only the income that falls above $30,000 is taxed at 20%.

- Your income is divided into portions based on the bracket thresholds.

- Each portion is taxed at the rate corresponding to its bracket.

- The tax amounts for each portion are added together to determine your total tax liability.

Example of Tax Bracket Calculation

Let's illustrate with a simplified example. Suppose the tax brackets are: 0-10,000 (10%), 10,001-30,000 (15%), 30,001-50,000 (20%), and above 50,000 (25%). If your taxable income is $40,000, the calculation would be:

- $10,000 taxed at 10% = $1,000

- $20,000 taxed at 15% = $3,000

- $10,000 taxed at 20% = $2,000

- Total tax = $1,000 + $3,000 + $2,000 = $6,000

Tax Brackets and Tax Liability

It's crucial to remember that even though you fall into a higher tax bracket, you don't pay that rate on your entire income. Only the portion of your income within that bracket is taxed at the higher rate. The lower portions of your income are still taxed at the lower rates of the previous brackets. This system is designed to be progressive, meaning higher earners pay a larger share of their income in taxes, but the marginal rates offer a degree of protection against extremely high tax burdens for small increases in income.

- The tax system isn't designed to punish higher earners for crossing bracket thresholds.

- It's a tiered system that assesses tax progressively, not proportionally.

- The effective tax rate (total tax/total income) will always be lower than the marginal tax rate for the highest bracket unless all your income falls within that single bracket.

How do I calculate my tax bracket?

What expenses can I deduct from my taxes?

What expenses can I deduct from my taxes?Calculating Your Tax Bracket

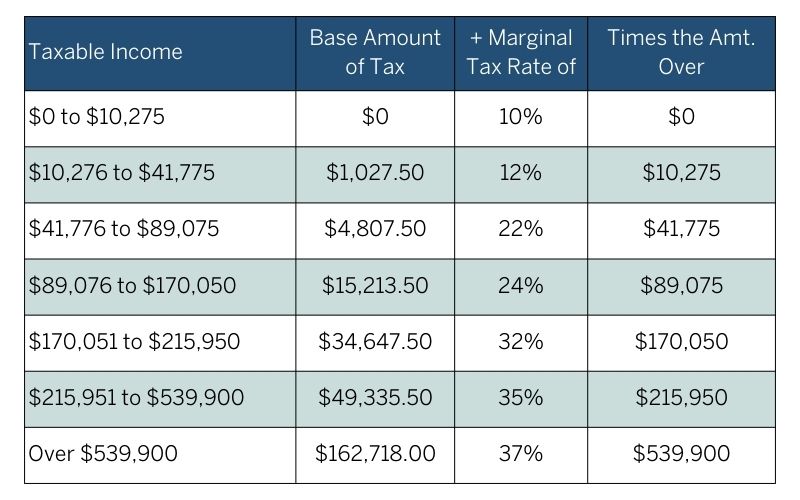

Calculating your tax bracket involves determining the range of taxable income that corresponds to a specific tax rate. This isn't a simple calculation of a single percentage applied to your entire income. Instead, tax systems, like those in the US, employ a progressive tax system. This means different portions of your income are taxed at different rates. To find your tax bracket, you'll need to refer to the applicable tax brackets published by your country's tax authority (e.g., the Internal Revenue Service (IRS) in the United States, or Her Majesty's Revenue and Customs (HMRC) in the United Kingdom). These brackets are usually presented in tables that specify income ranges and their corresponding marginal tax rates. You find the income range which contains your taxable income, and that range defines your tax bracket. Your total tax liability isn't simply your total income multiplied by your highest tax bracket percentage; instead, each portion of your income is taxed at its corresponding rate.

1. Understanding Tax Brackets and Marginal Tax Rates

Tax brackets represent ranges of taxable income, each subject to a different marginal tax rate. The marginal tax rate is the tax rate applied to the next dollar of income you earn. It's crucial to understand that your marginal tax rate is not the rate applied to your entire income. For example, if you fall into the 22% tax bracket, this doesn't mean 22% of your entire income is taxed at that rate. Only the portion of your income that falls within the 22% bracket is taxed at that rate. The portions falling within lower brackets are taxed at their respective lower rates. This progressive structure ensures that higher earners pay a larger percentage of their income in taxes.

- Locate the official tax brackets for your country and tax year. This information is usually available on the government's tax website.

- Identify the bracket(s) into which your taxable income falls. This may involve multiple brackets if your income exceeds the upper limit of a lower bracket.

- Calculate your tax liability for each bracket. Multiply the income within each bracket by that bracket's tax rate, then add these results together for your total tax liability.

2. Determining Your Taxable Income

Before you can find your tax bracket, you must calculate your taxable income. This isn't necessarily your gross income (your total income before deductions). Taxable income is determined after accounting for various deductions and adjustments. These deductions and adjustments vary depending on your individual circumstances and tax laws. Some common examples include standard deductions, itemized deductions, and adjustments to income like contributions to retirement accounts. Accurately calculating your taxable income is essential for correct bracket determination.

This content may interest you! How do self-employed individuals pay taxes?

How do self-employed individuals pay taxes?- Start with your gross income from all sources (wages, salaries, investments, etc.).

- Subtract any eligible above-the-line deductions. These are deductions subtracted directly from your gross income before you arrive at your adjusted gross income (AGI).

- Calculate your adjusted gross income (AGI). This is your gross income minus above-the-line deductions.

- Subtract below-the-line deductions such as the standard deduction or itemized deductions (whichever is greater). This results in your taxable income.

3. Using Tax Software or Professional Assistance

Calculating your tax bracket and overall tax liability can be complex, especially with intricate deductions and adjustments. Tax software programs or consulting a tax professional can simplify the process. Tax software provides step-by-step guidance, automatically calculates your taxable income, determines your tax bracket, and computes your overall tax liability. A tax professional can offer personalized advice and navigate complexities that might be challenging to handle independently. This is particularly beneficial for individuals with complicated tax situations, such as self-employment income, significant investment income, or international income.

- Explore reputable tax software options. Many offer free versions for simple tax situations and paid versions for more complex scenarios.

- Consult a tax accountant or enrolled agent if you need personalized assistance or have a complex tax situation.

- Carefully review all calculations and ensure accuracy before filing your taxes.

What does 22% tax bracket mean?

22% Tax Bracket Explained

A 22% tax bracket means that your taxable income falls within a specific range where the federal government taxes a portion of that income at a 22% rate. It's important to understand that this doesn't mean all of your income is taxed at 22%. Instead, it refers to the marginal tax rate applied to the portion of your income that falls within that particular bracket. The tax brackets are progressive, meaning higher income levels are taxed at higher rates. You still pay taxes on income in lower brackets at their respective rates, before reaching the 22% bracket.

This content may interest you! What is tax withholding and how does it affect my paycheck?

What is tax withholding and how does it affect my paycheck?How the 22% Tax Bracket Works

The 22% tax bracket is one of several marginal tax rates in the US federal income tax system. Your total tax liability is calculated by applying the different rates to the different portions of your income, each corresponding to its relevant bracket. The specific income thresholds that define each tax bracket change yearly and depend on your filing status (single, married filing jointly, etc.). Only the income that falls within the 22% bracket is subject to the 22% tax rate; income below that threshold is taxed at lower rates. Tax software or tax professionals can help determine your precise tax liability.

- Taxable Income: This is your gross income after subtracting certain deductions and adjustments.

- Marginal Rate: The 22% is the marginal tax rate, meaning it's the rate applied to the next dollarearned within that income bracket.

- Progressive System: The system is progressive because higher income levels are subject to increasingly higher tax rates. This ensures that higher earners contribute a larger percentage of their income to taxes compared to lower earners.

Examples of Income in the 22% Tax Bracket

The exact income range for the 22% tax bracket varies based on your filing status and the tax year. For example, in a given year, a single filer might be in the 22% bracket if their taxable income is between $44,725 and $95,375. A married couple filing jointly might have a different range entirely. Consult the IRS Publication 17 (Your Federal Income Tax) for the most up-to-date brackets applicable to your situation. It’s crucial to check the current IRS guidelines as brackets change annually due to inflation adjustments and potential legislative changes.

- Single Filers: The income range for single filers falling under the 22% tax bracket will differ from year to year.

- Married Filing Jointly: The income range for married couples filing jointly will also vary annually and be different than the range for single filers.

- Head of Household: Taxpayers filing as Head of Household will have yet another range, specific to this filing status.

Tax Credits and Deductions in the 22% Tax Bracket

Tax credits and deductions can significantly impact your overall tax liability, even if you're in the 22% tax bracket. Tax credits directly reduce the amount of tax you owe, dollar for dollar, while deductions reduce your taxable income. Because of this, deductions benefit higher income individuals more due to the progressive tax system. Therefore, maximizing eligible credits and deductions is essential for taxpayers at every income level, including those in the 22% bracket, potentially lowering their tax burden. This is where professional tax advice can be incredibly valuable.

- Tax Credits: Directly reduce your tax bill. Examples include the Child Tax Credit and Earned Income Tax Credit.

- Tax Deductions: Reduce your taxable income. Examples include deductions for charitable contributions, mortgage interest, and state and local taxes (depending on limitations).

- Itemized vs. Standard Deduction: Depending on your specific deductions, itemizing might lower your taxable income more than taking the standard deduction. It's important to calculate both to determine which yields the most significant tax savings.

What is my tax bracket if I make $60,000?

How to save money if you don't have a job?

How to save money if you don't have a job?Determining your exact tax bracket requires knowing several factors beyond just your income. The $60,000 figure is your gross income, but your taxable income will be lower after deductions and adjustments. Tax brackets also vary by filing status (single, married filing jointly, etc.) and the year. Therefore, I cannot definitively state your tax bracket. To find your precise tax bracket, you should consult the IRS tax tables for the relevant tax year or use tax software. These resources will calculate your taxable income and the applicable tax rates based on your specific situation.

What are the Federal Income Tax Brackets?

The federal income tax system in the United States is progressive, meaning higher earners pay a larger percentage of their income in taxes. The tax brackets are ranges of income that are subject to different tax rates. For example, a single filer in a given year might find that income from $0 to $10,000 is taxed at 10%, income from $10,001 to $40,000 is taxed at 12%, and so on. It is important to remember that this only means that the portionof your income within a specific bracket is taxed at that rate; it doesn't mean your entire income is taxed at that highest rate. The higher your income, the more brackets are applicable.

- You will pay the tax rate for each bracket your income falls into.

- The tax rates change periodically, so always check for updates.

- Tax software or a tax professional can help determine your specific tax liability.

How Do Deductions and Adjustments Affect My Tax Bracket?

Deductions and adjustments to income lower your taxable income. Common deductions include those for mortgage interest, charitable contributions, and state and local taxes (depending on limitations). Adjustments can include things like contributions to a health savings account (HSA) or traditional IRA. These reductions can significantly impact which tax bracket you fall into, potentially moving you to a lower bracket and reducing your overall tax liability. It's crucial to accurately account for all eligible deductions and adjustments when calculating your taxes.

- Itemized deductions may lower your taxable income more than the standard deduction.

- Adjustments to income reduce your gross income before calculating your taxable income.

- Accurately claiming all applicable deductions and adjustments is essential.

What Other Taxes Might Apply Besides Federal Income Tax?

Beyond federal income tax, there are other taxes you may need to consider, including state and local income taxes (depending on your location), Social Security and Medicare taxes (FICA), and potentially property taxes. State and local income tax rates vary considerably, and understanding these obligations is just as critical as understanding your federal obligations. Remember that these taxes, while seemingly separate from your federal income tax bracket, are still a factor in determining your overall tax liability and financial planning.

This content may interest you! What are taxes and how do they work?

What are taxes and how do they work?- State and local taxes can add significantly to your overall tax burden.

- FICA taxes are deducted from your paycheck and are based on a percentage of your earnings.

- Consult with a tax professional or utilize tax software to determine all applicable taxes.

What are tax brackets?

Tax brackets are ranges of income that are taxed at different rates. The more you earn, the higher the tax bracket you fall into. However, this doesn't mean your entire income is taxed at the highest rate. Only the portion of your income that falls within a specific bracket is taxed at that bracket's rate. For example, if you have a $50,000 income and the bracket is $40,000-$80,000 at 20%, only the income above $40,000 is taxed at 20%. The income below remains taxed at a lower rate. The system is progressive, meaning higher earners pay a larger percentage of their income in taxes.

How is my tax calculated using brackets?

Your tax isn't simply calculated by multiplying your total income by the highest bracket's rate. Instead, a progressive system is applied. Each portion of your income within a specific bracket is taxed at that bracket's rate. The tax amounts for each bracket are then added together to arrive at your total tax liability. Tax software or professional tax advisors can easily calculate this for you. Understanding how the brackets work helps you predict your tax burden and make informed financial decisions. This ensures fairness across different income levels.

Do tax brackets change?

Yes, tax brackets are adjusted periodically, usually annually. These adjustments are influenced by factors like inflation and legislative changes. Governments may increase or decrease tax rates or adjust the income thresholds defining each bracket. Keeping up-to-date with these changes is crucial for accurate tax planning. Tax laws vary between countries, so it's vital to check your country's specific guidelines and rates for the current year. Changes are typically announced by tax agencies before the tax filing season.

Are there different tax brackets for different filing statuses?

Yes, absolutely. Tax brackets are usually structured to accommodate different filing statuses, such as single, married filing jointly, married filing separately, and head of household. Each filing status has its own set of brackets with varying income thresholds and tax rates. Your marital status and dependents significantly influence which brackets apply to you, leading to different tax liabilities even with similar incomes. It’s important to select the correct filing status when completing your tax return to ensure accurate calculations and avoid potential penalties.

Leave a Reply