Can you start investing at a young age?

Investing might seem daunting, especially when you're young and just starting out. But the truth is, beginning your investment journey early offers significant advantages. This article explores the benefits of starting young, addressing common concerns like lack of capital and understanding the market.

We'll delve into various investment options suitable for young investors, emphasizing the power of compounding and long-term growth. Discover how even small, consistent contributions can build substantial wealth over time, setting you up for financial security in your future.

Investing Early: Unlocking the Power of Compound Interest

Yes, absolutely! Starting to invest at a young age offers a significant advantage, primarily due to the magic of compound interest. This means that your earnings generate further earnings over time. The earlier you start, the longer your money has to grow exponentially.

Even small, consistent contributions made during your younger years can accumulate into a substantial sum by the time you reach retirement or other financial goals. This allows for greater flexibility in your later life, reducing the pressure to work solely for income and providing more choices regarding career paths, lifestyle, and overall financial security.

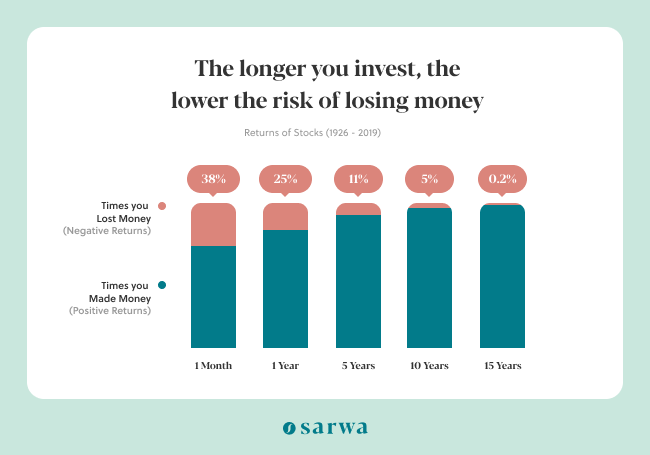

Furthermore, young investors often have a longer time horizon to ride out market fluctuations, making them less susceptible to short-term market volatility and potentially benefiting from long-term growth.

Understanding Your Risk Tolerance

As a young investor, you generally have a higher risk tolerance than someone closer to retirement. This is because you have more time to recover from potential losses. You can afford to invest in assets with higher growth potential, even if they carry greater risk, such as stocks or growth-oriented mutual funds.

However, it's crucial to still conduct thorough research and understand the potential downsides before investing your money.

Diversification is key to mitigating risk; don't put all your eggs in one basket. Learning about different investment strategies and asset classes is paramount before committing funds. Gradually increasing your investment knowledge and experience over time is a smart approach.

Small Investments, Big Returns: The Power of Consistent Contributions

You don't need a large sum of money to start investing. Many platforms allow you to begin with very small, regular contributions. The key is consistency. Even small, regular investments, such as $50 or $100 per month, can add up significantly over time thanks to the power of compounding.

Consider setting up automatic transfers from your checking account to your investment account to ensure regular contributions without having to actively think about it each month. This method of dollar-cost averaging helps to mitigate the risk of investing a lump sum at a market high.

Available Investment Options for Young Investors

The investment landscape offers a wide variety of options suitable for young investors. Retirement accounts like 401(k)s and IRAs provide significant tax advantages, making them excellent choices for long-term growth.

This content may interest you! Is investing young smart?

Is investing young smart?Index funds and exchange-traded funds (ETFs) offer diversified exposure to a broad market segment at low costs. Individual stocks can offer higher growth potential but carry increased risk. It's crucial to choose investments aligned with your risk tolerance, financial goals, and investment timeline.

Consider consulting with a financial advisor to determine which options best suit your individual needs.

| Investment Type | Risk Level | Potential Return | Time Horizon |

|---|---|---|---|

| High-yield Savings Account | Low | Low | Short-term |

| Bonds | Medium | Medium | Medium-term |

| Stocks | High | High | Long-term |

| Real Estate | Medium-High | Variable | Long-term |

Is it good to start investing at a young age?

Yes, starting to invest at a young age offers significant advantages. The primary benefit is the power of compounding. This means that your initial investment earns returns, and those returns then earn further returns over time.

The longer your money has to grow, the more substantial the effect of compounding becomes. This allows your investments to grow exponentially, potentially leading to a significantly larger nest egg by the time you retire compared to someone who starts investing later in life.

Even small, consistent contributions made early on can accumulate to a considerable sum due to the extended time horizon. Furthermore, younger investors generally have a higher risk tolerance and a longer time horizon to recover from potential market downturns, allowing them to potentially benefit from higher-return, higher-risk investments.

Starting early also instills valuable financial habits and knowledge that can benefit you throughout your life.

The Power of Compounding

The magic of compounding is perhaps the most compelling reason to start investing early. It's the snowball effect of earning returns on your returns. Imagine investing $100 at a 7% annual return. After 10 years, it grows to $196.72.

However, if you continue investing for another 30 years, it grows to $761.23. The later years' growth is significantly larger. This illustrates the exponential growth potential. The longer your money is invested, the more it grows, and the larger the impact of compounding becomes.

- Early investment maximizes the compounding effect, allowing your money to grow exponentially over time.

- Even small, consistent contributions made early on can accumulate to a considerable sum due to the extended time horizon.

- The longer you invest, the more significant the impact of compounding, even with modest returns.

Higher Risk Tolerance and Longer Time Horizon

Younger investors typically possess a higher risk tolerance. This is because they have more time to recover from potential market downturns. They can afford to allocate a larger portion of their portfolio to higher-risk, higher-return investments such as stocks. This increased risk appetite allows for potentially greater returns over the long term.

The extended time horizon enables investors to ride out market fluctuations without the urgent need to liquidate assets at inopportune times.

This content may interest you! How to invest in your 50s in the UK?

How to invest in your 50s in the UK?- A longer time horizon allows for recovery from market downturns and greater exposure to higher-return investments.

- Higher risk tolerance can translate to higher potential returns over the long term.

- Younger investors are less likely to panic-sell during market corrections due to the extended time before needing their investments.

Developing Financial Habits and Knowledge

Starting to invest early on fosters valuable financial literacy and discipline. It encourages responsible saving and planning for the future. The process of researching investments and monitoring portfolios builds essential financial skills.

This knowledge and experience become increasingly valuable as you navigate different life stages and financial goals. Early investment instills good habits that can positively influence other areas of your personal finances.

- Early investment encourages saving habits and responsible financial planning.

- The process builds essential financial literacy and knowledge.

- This experience and knowledge can positively impact other areas of personal finance throughout life.

How much is $1000 a month for 5 years?

$1000 a month for 5 years is a total of $60,000. This is calculated by multiplying the monthly amount by the number of months in a year (12) and then multiplying that by the number of years (5): $1000/month 12 months/year 5 years = $60,000.

Calculating the Total Amount

To determine the total amount of money accumulated over five years with a consistent monthly payment of $1000, a straightforward calculation is necessary. This involves multiplying the monthly payment by the total number of months in the five-year period. This method provides a clear and concise understanding of the overall financial commitment or accumulation.

- Determine the number of months: 5 years 12 months/year = 60 months

- Multiply the monthly payment by the total number of months: $1000/month 60 months = $60,000

- The total amount accumulated over 5 years is $60,000.

Factors Affecting the Real Value

While the calculation above gives a nominal value, the real value of $60,000 over five years is affected by inflation. Inflation erodes the purchasing power of money over time, meaning that $60,000 in five years will likely buy less than $60,000 today. Other factors, like investment returns if the money is saved, also affect the ultimate value.

- Inflation: The rate of inflation will reduce the real value of the $60,000 over time.

- Investment Returns: If the $1000 monthly payments are invested, the final value will be greater than $60,000, depending on the investment returns.

- Taxes: Taxes on earnings or investments will also impact the final amount.

Applications of this Calculation

This simple calculation has broad applications in personal finance and business. It's useful for budgeting, saving goals, loan repayments, and investment projections. Understanding this fundamental calculation allows for better financial planning and decision-making.

- Budgeting: Determining if a $1000 monthly expense is feasible within a larger budget.

- Saving Goals: Tracking progress toward a savings goal of $60,000 in five years.

- Loan Repayments: Calculating the total repayment amount for a loan with $1000 monthly payments over five years.

How to invest $1000 for a child?

Investing $1000 for a child can be a great way to start building their financial future. The best approach depends on the child's age, your risk tolerance, and your investment timeline. Generally, longer time horizons allow for more aggressive investment strategies, while shorter time horizons often necessitate a more conservative approach.

There are several options available, each with its own pros and cons. Careful consideration of these factors will help you make an informed decision.

Custodial Accounts

A custodial account, such as a Uniform Gift to Minors Act (UGMA) or Uniform Transfers to Minors Act (UTMA) account, is a popular choice for investing for children.

This content may interest you! What should a 55 year old invest in?

What should a 55 year old invest in?These accounts allow you to manage the investments on behalf of the child until they reach the age of majority (typically 18 or 21, depending on the state). The assets in the account belong to the child, and they will have complete control over them once they reach the age of majority.

This offers a simple, straightforward way to begin investing, but requires careful thought regarding the potential use of funds by the child upon reaching legal age.

- Simplicity: Relatively easy to set up and manage.

- Tax Advantages: Investment earnings are taxed at the child's rate, which might be lower than yours.

- Ownership: The assets ultimately belong to the child.

529 Education Savings Plans

A 529 plan is a tax-advantaged savings plan designed specifically for education expenses. Contributions aren't tax-deductible at the federal level (though some states offer deductions), but the earnings grow tax-deferred, and withdrawals used for qualified education expenses are tax-free.

This makes it an ideal choice if you are saving specifically for college or other post-secondary education. However, if the child doesn't pursue higher education, withdrawing the funds for other purposes will incur taxes and penalties.

- Tax Advantages: Earnings grow tax-deferred and withdrawals for qualified education expenses are tax-free.

- Flexibility: Many plans offer a variety of investment options.

- State Benefits: Some states offer tax deductions or other incentives for contributing to their 529 plans.

Roth IRAs (for the Child's Future)

While a Roth IRA is typically associated with retirement savings, contributing to one for a child (under certain circumstances, if they have earned income) is possible. This provides the long-term benefit of tax-free withdrawals during retirement.

Contributions are made with after-tax dollars, but qualified withdrawals in retirement are entirely tax-free. However, the rules are complex and the child must meet specific requirements regarding earned income to be eligible. Investing early in a Roth IRA is a potent long-term strategy, though more complex than other methods.

- Tax-Free Growth: Investments grow tax-free.

- Tax-Free Withdrawals: Withdrawals in retirement are tax-free.

- Eligibility Requirements: The child must have earned income to contribute.

How much will $100 a month be worth in 30 years?

:max_bytes(150000):strip_icc()/Clipboard03-df27c0eb3ccf470a9a424dbc0a13d93b.png)

Calculating the future value of a $100 monthly investment over 30 years requires considering several factors, primarily the rate of return (interest rate). There's no single answer without specifying an assumed annual rate of return.

The calculation uses the future value of an ordinary annuity formula. Different investment vehicles will offer different rates of return, ranging from relatively low-risk options like savings accounts to higher-risk options such as stocks.

The higher the assumed annual rate of return, the higher the future value will be. To illustrate, we'll provide examples with different rates.

Assumptions and Variables

To accurately determine the future value, we need to make some assumptions. The most critical assumption is the average annual rate of return. This is a crucial factor because it directly impacts the final value of the investment.

This content may interest you! How much should a 50 year old have in savings UK?

How much should a 50 year old have in savings UK?We'll show examples with conservative and more aggressive return assumptions. Other factors that can influence the final amount include fees associated with the investment account, whether or not taxes are accounted for, and the consistency of the $100 monthly contribution.

It's important to remember that past performance is not indicative of future results.

- Annual Rate of Return: This is the percentage your investment grows each year. Different investments have different potential rates of return.

- Investment Period: In this case, it's 30 years.

- Monthly Contribution: A consistent $100 monthly investment.

Calculating Future Value with Different Rates of Return

The future value of an ordinary annuity formula is used to calculate this. The formula is complex, but financial calculators or spreadsheet software can easily handle it. Let's examine scenarios using different rates:

- Conservative Estimate (5% annual return): At a modest 5% annual return, a $100 monthly investment over 30 years would grow to approximately $100,000. This return rate may be found in low-risk investment vehicles. This is an approximation and can vary depending on the compounding frequency (monthly, quarterly, annually).

- Moderate Estimate (7% annual return): A 7% annual return, often achievable with a diversified portfolio of stocks and bonds, could result in a future value closer to $160,000 after 30 years. This is still a generalized estimate.

- Aggressive Estimate (10% annual return): A 10% annual return is a more aggressive projection. While possible, it's important to recognize the higher risk associated with achieving this rate. With a 10% annual return, the investment could accumulate to approximately $250,000 or more after 30 years. This requires a significant level of risk taking.

Factors Affecting the Final Value

The calculated future values above are estimates. Several factors can influence the actual outcome. It's essential to consider these variables when planning long-term investments. Remember that market fluctuations can significantly impact returns over a 30-year period.

- Inflation: The purchasing power of $250,000 in 30 years will likely be lower than the purchasing power of that same amount today due to inflation.

- Fees: Investment fees and taxes can significantly reduce your final returns. Always factor these costs into your projections.

- Market Volatility: The stock market experiences ups and downs. Your actual returns may be higher or lower than the projections based on market conditions.

Frequently Asked Questions

What are the benefits of starting to invest young?

Starting to invest young offers several key advantages. The most significant is the power of compounding. The longer your investments have to grow, the more time they have to generate returns that themselves generate further returns.

This snowball effect significantly increases your wealth over time compared to starting later. Additionally, younger investors typically have a longer time horizon, allowing them to weather market downturns more easily without needing to withdraw funds prematurely. Finally, even small, regular investments made early can accumulate into a substantial sum over decades.

What are some suitable investment options for young adults?

Several investment options are suitable for young adults, depending on their risk tolerance and financial goals. Low-cost index funds and exchange-traded funds (ETFs) are excellent choices, providing diversification and generally strong long-term returns.

Individual stocks can also be a viable option, but require more research and understanding of the market. For beginners, robo-advisors offer automated portfolio management, simplifying the investment process.

High-yield savings accounts and certificates of deposit (CDs) provide lower returns but offer greater security for a portion of savings. The best approach is often a diversified strategy across different asset classes.

How much money do I need to start investing?

You don't need a large sum of money to start investing. Many brokerage accounts have no minimum investment requirements, allowing you to invest as little as a single share of a stock or a small amount in a mutual fund.

Dollar-cost averaging, a strategy of investing a fixed amount at regular intervals, is particularly beneficial for beginners with limited funds. This approach mitigates the risk of investing a lump sum at a market high.

This content may interest you! Is saving $1000 a month good in the UK?

Is saving $1000 a month good in the UK?Even small, consistent contributions over time can lead to significant growth due to compounding returns. Consider starting with a small amount and gradually increasing contributions as your income grows.

What are the risks associated with investing at a young age?

While starting young offers significant advantages, investing does involve risks. Market volatility is a key concern, meaning the value of your investments can fluctuate significantly, potentially leading to losses in the short term.

However, for long-term investors, these fluctuations are generally less concerning. Another risk is emotional decision-making, especially during market downturns. It's crucial to avoid impulsive actions based on fear or panic.

Educating yourself about investing, understanding your risk tolerance, and having a long-term perspective can help mitigate these risks. Diversification across asset classes further reduces overall risk.

Leave a Reply