How to pay $30,000 debt in one year?

Facing a $30,000 debt can feel overwhelming, but with a strategic plan and unwavering commitment, it's possible to conquer it within a year. This article outlines a practical, step-by-step guide to aggressively tackle your debt. We'll explore effective budgeting techniques, explore debt consolidation options, and discuss strategies for increasing your income. Prepare to learn how to prioritize your payments, negotiate with creditors, and develop a sustainable financial plan to achieve your debt-free goal within twelve months. Let's get started on your journey to financial freedom.

Aggressive Strategies for Eliminating a $30,000 Debt in One Year

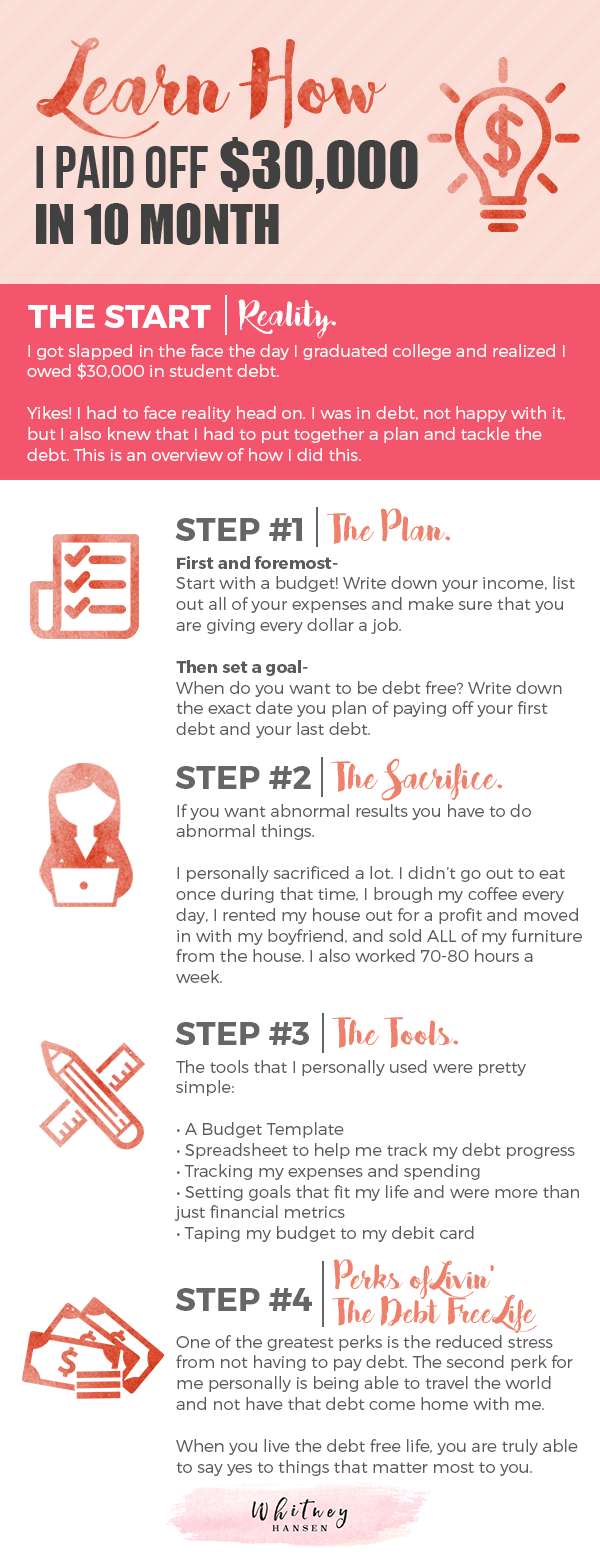

Paying off $30,000 in debt within a year is an ambitious goal, requiring significant commitment and potentially drastic lifestyle changes. It's crucial to understand that this isn't feasible for everyone, and success depends heavily on your current financial situation, income, and access to resources. However, with a well-structured plan and unwavering dedication, it's possible. The core strategy relies on maximizing income while minimizing expenses, and strategically attacking the debt. This often means making sacrifices and prioritizing debt repayment above all else. Consider exploring options like side hustles, selling assets, and negotiating lower interest rates. Remember to meticulously track your progress to stay motivated and ensure you're on track to reach your goal. Financial counseling can be invaluable in developing a personalized plan and navigating potential challenges.

Creating a Realistic Budget and Identifying Areas for Savings

The first step in tackling a $30,000 debt is creating a detailed budget that accurately reflects your income and expenses. Track every dollar you earn and spend for at least a month to get a clear picture of your financial situation. Identify areas where you can drastically cut back on spending. This could involve reducing dining out, canceling subscriptions, finding cheaper housing, or limiting entertainment expenses. Prioritize essential expenses such as housing, food, and transportation, and be ruthless in eliminating non-essential spending. The key is to create a significant surplus each month that can be directed towards debt repayment. Consider using budgeting apps or spreadsheets to track your progress and maintain financial clarity.

Exploring Debt Consolidation and Refinancing Options

Debt consolidation and refinancing can be powerful tools in accelerating debt repayment. Debt consolidation involves combining multiple debts into a single loan, potentially with a lower interest rate. This simplifies payments and can streamline the repayment process. Refinancing can also lower your interest rate on existing debts, reducing the overall cost of borrowing and freeing up more money for principal repayment. Shop around for the best rates and terms from different lenders. Be aware of potential fees associated with these processes. Carefully consider the terms and conditions of any loan before committing, ensuring it aligns with your financial goals and avoids trapping you in a worse situation. Always read the fine print.

This content may interest you! What debt Cannot be erased?

What debt Cannot be erased?Increasing Your Income Through Side Hustles and Additional Income Streams

To accelerate debt repayment, you may need to significantly increase your income. Explore various side hustles that fit your skills and availability. This could include freelancing, gig work, selling items online, or taking on a part-time job. Diversifying your income streams reduces reliance on a single source and provides more flexibility to allocate funds towards debt. Be realistic about the time and effort required for these extra endeavors. Ensure the additional income generated significantly outweighs the time and effort invested, keeping the ultimate goal – debt elimination – in focus. Don’t overlook potential tax implications from additional income sources.

| Strategy | Description | Potential Benefits | Potential Drawbacks |

|---|---|---|---|

| Budgeting | Creating a detailed plan for income and expenses. | Increased savings and financial clarity. | Requires discipline and potentially significant lifestyle changes. |

| Debt Consolidation/Refinancing | Combining multiple debts or lowering interest rates. | Lower monthly payments and faster repayment. | Potential fees and risks associated with new loans. |

| Side Hustles | Generating additional income through part-time work. | Increased cash flow to accelerate debt repayment. | Requires extra time and effort; may impact personal life. |

How to pay off $30,000 debt fast?

How to Pay Off $30,000 Debt Fast?

Create a Realistic Budget and Stick to It

Paying off a significant debt like $30,000 requires a disciplined approach to your finances. A realistic budget is crucial. This involves tracking your income and expenses meticulously to understand where your money is going. Once you have a clear picture, identify areas where you can cut back on spending to free up more money for debt repayment. This might involve reducing subscriptions, dining out less, or finding cheaper alternatives for everyday expenses. Consistency is key; regularly reviewing and adjusting your budget is essential to stay on track.

- Track all income and expenses using budgeting apps or spreadsheets.

- Identify non-essential spending and eliminate or reduce it.

- Create a detailed budget allocating funds for debt repayment, essential expenses, and a small amount for savings.

Explore Debt Repayment Strategies

Several methods can accelerate your debt repayment. The debt avalanche method prioritizes paying off the highest-interest debt first, saving you money on interest in the long run. Alternatively, the debt snowball method focuses on paying off the smallest debt first for psychological motivation, boosting your confidence as you see progress. Consider consolidating your debt into a lower-interest loan or balance transfer credit card to simplify payments and potentially reduce interest charges. Each method has its advantages, and choosing the best approach depends on your personality and financial situation.

This content may interest you! How to pay off $50,000 in debt in 1 year?

How to pay off $50,000 in debt in 1 year?- Debt Avalanche: Prioritize debts with the highest interest rates.

- Debt Snowball: Prioritize debts with the smallest balance.

- Debt Consolidation: Combine multiple debts into a single loan or credit card.

Increase Your Income

While cutting expenses is vital, increasing your income can significantly shorten your debt repayment journey. Explore opportunities for a side hustle, like freelancing, gig work, or selling unused items. Consider asking for a raise at your current job or searching for a higher-paying position. Even small increases in income can make a big difference when consistently applied to debt repayment. Remember to be strategic and realistic in your approach to finding additional income streams.

- Explore freelance or gig work opportunities based on your skills.

- Negotiate a raise at your current job or actively search for higher-paying employment.

- Sell unused possessions or consider renting out a spare room or property.

How to pay 30k in a year?

Paying off $30,000 in a Year

Paying off $30,000 in a year requires a significant commitment and a well-structured plan. It's crucial to understand your current financial situation, including income, expenses, and existing debts. A debt snowball or avalanche method can be effective. The snowball method prioritizes paying off the smallest debts first for motivational purposes, while the avalanche method focuses on the debts with the highest interest rates to minimize overall interest paid. Consider consolidating high-interest debts into a lower-interest loan to simplify payments and potentially save money. Negotiating with creditors for lower interest rates or payment plans might also be possible. Remember that successful debt repayment necessitates consistent effort, discipline, and a realistic budget. Unexpected expenses can derail your progress, so having an emergency fund is highly recommended.

This content may interest you! How do I get out of owing money?

How do I get out of owing money?Creating a Realistic Budget

A meticulously crafted budget is paramount for successfully tackling a $30,000 debt. This involves tracking every expense, identifying areas for reduction, and allocating funds specifically towards debt repayment. Prioritizing essential needs over wants can free up significant resources. Exploring ways to increase income, such as taking on a part-time job or freelancing, can accelerate the repayment process. Careful budgeting not only aids in debt reduction but also cultivates responsible financial habits for long-term well-being.

- Track all income and expenses meticulously using budgeting apps or spreadsheets.

- Identify areas where you can cut expenses, such as subscriptions, entertainment, or dining out.

- Allocate a specific amount each month to debt repayment, ensuring it remains consistent.

Exploring Additional Income Streams

Supplementing your existing income is crucial when aiming to repay $30,000 in a short timeframe. Consider various options based on your skills and availability. Freelancing platforms offer opportunities to utilize your expertise for projects, while part-time jobs provide a steady supplemental income stream. Selling unused possessions or assets can generate immediate funds. Be mindful of the time commitment and potential impact on your primary job or responsibilities when choosing additional income streams. It is vital to ensure these new income sources are sustainable and don't compromise your overall well-being.

- Explore freelance opportunities on platforms like Upwork or Fiverr based on your skillset.

- Seek part-time employment opportunities that align with your schedule and abilities.

- Declutter your home and sell unwanted items online or at consignment shops.

Negotiating with Creditors

Direct communication with creditors can significantly impact your debt repayment journey. Negotiating lower interest rates can save you substantial amounts in interest charges over time. Exploring debt consolidation options can simplify payments and potentially reduce your monthly obligations. In some cases, creditors might be willing to work with you on a modified repayment plan, extending the repayment period or adjusting payment amounts. However, remember that any negotiated agreements will impact your credit score, and documentation of these changes is crucial.

- Contact your creditors and explain your situation, outlining your intention to repay the debt.

- Inquire about potential interest rate reductions or modified payment plans.

- Consider consolidating high-interest debts into a lower-interest loan to simplify payments.

How many years will it take to pay off $30000?

How do I clear my bank debt?

How do I clear my bank debt?Paying Off $30,000

There's no single answer to how many years it will take to pay off $30,000. The time required depends entirely on several key factors:

Interest Rate

The interest rate significantly impacts the repayment timeline. A higher interest rate means more of your payments go towards interest, leaving less to reduce the principal balance. This results in a longer repayment period. Conversely, a lower interest rate allows you to pay off the debt faster.

- High interest rates (e.g., above 15%): Expect a longer repayment period, potentially several years longer than with lower rates.

- Moderate interest rates (e.g., 5-10%): Repayment will likely take several years, depending on the payment amount.

- Low interest rates (e.g., below 5%): You can expect a shorter repayment period, potentially significantly shorter than with higher rates.

Monthly Payment Amount

The amount you pay monthly directly influences how quickly you eliminate the debt. Larger monthly payments dramatically reduce the principal balance faster, leading to a shorter repayment period. Smaller payments extend the repayment timeline considerably due to accumulating interest.

This content may interest you! Is $20,000 a lot of debt?

Is $20,000 a lot of debt?- High monthly payments: Significantly shorten repayment time, potentially allowing for debt elimination within a few years.

- Moderate monthly payments: Result in a moderate repayment time frame, likely spanning several years.

- Low monthly payments: Will extend the repayment period substantially, possibly taking a decade or more.

Payment Frequency

While monthly payments are common, more frequent payments (e.g., bi-weekly or weekly) accelerate debt repayment. Each additional payment reduces the principal and the total interest accrued over the loan's life, ultimately shortening the total repayment time. This is because you pay off a portion of the interest more often.

- Monthly payments: The most common, leading to a repayment period that depends on the interest rate and the payment amount.

- Bi-weekly payments: Accelerates the payoff, typically resulting in a shorter repayment period than monthly payments.

- Weekly payments: The most aggressive approach, significantly shortening the repayment timeline.

How to pay off a $30,000 loan fast?

Paying Off a $30,000 Loan Fast

How to Pay Off a $30,000 Loan Fast?

Paying off a $30,000 loan quickly requires a multifaceted approach combining aggressive repayment strategies with careful financial management. There's no magic bullet, but a combination of the following tactics can significantly shorten your repayment timeline. The key is to increase your payments as much as possible while simultaneously reducing your expenses and exploring opportunities to increase your income. The more you can pay above the minimum payment, the faster you'll become debt-free. Remember to always check with your lender before making extra payments to ensure there are no prepayment penalties.

This content may interest you! What to do if you are in massive debt?

What to do if you are in massive debt?Increase Your Payments

The most direct way to pay off a loan faster is to increase your monthly payments. This can be done in several ways. Even small increases over time can make a big difference in reducing the total interest paid and the overall loan term. Consider the following:

- Make bi-weekly payments: Instead of one monthly payment, make half your monthly payment every two weeks. This translates to one extra monthly payment per year.

- Make lump-sum payments: Whenever possible, apply extra funds towards the principal balance. This could include tax refunds, bonuses, or unexpected income.

- Refinance to a lower interest rate: A lower interest rate can significantly reduce your monthly payment or allow you to allocate more towards the principal without increasing your monthly outflow. Shop around for better rates and consider refinancing to a shorter term.

Reduce Expenses and Increase Income

To free up more money for loan repayment, you need to control spending and look for ways to earn more. This involves a thorough review of your budget and lifestyle. Small changes can add up significantly over time. Consider:

- Create a detailed budget: Track your income and expenses meticulously to identify areas where you can cut back. Subscription services, dining out, and entertainment are common areas for potential savings.

- Negotiate lower bills: Contact your service providers (internet, phone, insurance) to negotiate lower rates or explore cheaper alternatives.

- Find extra income sources: This could involve a part-time job, freelancing, selling unused possessions, or renting out a spare room.

Debt Consolidation and Balance Transfers

Consolidating your debt into a single loan with a lower interest rate can simplify your payments and potentially reduce your overall interest costs. Balance transfers to a credit card with a 0% introductory APR can also be a useful tool, but be aware of the potential for high interest rates after the introductory period expires. Careful planning and discipline are crucial for successfully using this method.

- Compare interest rates: Research different lenders and credit cards to find the lowest interest rate available to you.

- Understand the terms and conditions: Pay close attention to fees, interest rate changes after the introductory period, and any potential penalties.

- Develop a repayment plan: Create a realistic budget and stick to it to ensure you repay the debt before the introductory period ends, or your rate increases.

Is it even possible to pay off a $30,000 debt in one year?

While challenging, it's certainly possible for some individuals. Success depends heavily on your current income, expenses, and the interest rate on your debt. A rigorous budget, aggressive debt repayment strategies (like the debt snowball or avalanche methods), and potentially additional income streams are crucial. The higher your income and the lower your interest rate, the more feasible this goal becomes. It requires significant commitment and discipline, but it can be achieved with careful planning and execution.

This content may interest you! How can I save money if I have debt?

How can I save money if I have debt?What debt repayment strategies are most effective for a $30,000 debt?

The debt avalanche method prioritizes paying off high-interest debts first to minimize total interest paid, while the debt snowball method focuses on paying off the smallest debts first for psychological motivation. Both are effective; choose the one that best suits your personality and financial situation. Consider consolidating your debts into a lower-interest loan to simplify payments and potentially reduce interest charges. Negotiating with creditors for lower interest rates or payment plans can also significantly impact your ability to pay off the debt faster.

How can I increase my income to accelerate debt repayment?

Explore all avenues to boost your earnings. This could involve taking on a part-time job, freelancing, selling unused possessions, or monetizing skills through online platforms. Consider negotiating a raise at your current job or searching for a higher-paying position. If you have assets that appreciate in value, explore ways to leverage them for additional income, always carefully considering the risks involved. Every extra dollar contributes to accelerating your debt repayment journey.

What are the potential downsides of aggressively paying off debt in one year?

While rapid debt repayment offers significant long-term benefits, it can create short-term sacrifices. Aggressively cutting expenses might limit your ability to enjoy life, impacting your mental and emotional wellbeing. Ignoring essential spending (like health insurance or car maintenance) could lead to more significant financial problems down the line. It’s vital to find a balance between aggressive debt repayment and maintaining a healthy lifestyle to avoid burnout and unexpected financial emergencies.

Leave a Reply