What is the 70/30 rule in investing?

The 70/30 rule, a popular investment guideline, suggests allocating 70% of your portfolio to stable, lower-risk investments and 30% to higher-risk, potentially higher-return assets. This balanced approach aims to mitigate risk while still allowing for growth potential.

This article delves into the specifics of the 70/30 rule, exploring its benefits, drawbacks, and considerations for different investor profiles and risk tolerances. We'll examine how to implement this strategy effectively and whether it's the right approach for your personal financial goals.

What is the 70/30 Rule in Investing?

The 70/30 rule in investing is a simple asset allocation strategy that suggests dividing your investment portfolio into two main categories: 70% in conservative investments and 30% in growth investments. This rule acts as a guideline to balance risk and reward.

The specific breakdown of these percentages can be adjusted based on your individual risk tolerance, time horizon, and financial goals. It is crucial to understand that this is a rule of thumb, not a rigid prescription, and professional financial advice should always be sought before making any significant investment decisions.

The core concept is to secure a base of relatively stable assets while still allowing for potential higher returns from growth-oriented investments.

What are Considered Conservative Investments?

Conservative investments, representing the 70% portion of the 70/30 rule, generally focus on capital preservation and lower risk. These typically include options like high-yield savings accounts, certificates of deposit (CDs), money market accounts, and government bonds.

The emphasis is on minimizing the chance of losing principal, even if the potential returns are more modest compared to riskier assets. These investments offer stability and liquidity, making them suitable for securing a portion of your portfolio and protecting your initial investment.

What are Considered Growth Investments?

Growth investments, making up the remaining 30% in the 70/30 rule, prioritize potential higher returns. These are typically considered higher-risk investments, and include assets like stocks, real estate, and alternative investments (e.g., private equity, hedge funds). While offering the possibility of significant capital appreciation, these investments are more susceptible to market fluctuations and potential losses.

This content may interest you! Can you start investing at a young age?

Can you start investing at a young age?The allocation to growth investments should reflect your risk tolerance and your investment time horizon; a longer time horizon generally allows for greater exposure to riskier growth-oriented assets.

How to Adjust the 70/30 Rule Based on Your Circumstances?

The 70/30 rule is a flexible guideline, not a strict law. Your age, risk tolerance, and investment goals should inform the optimal asset allocation for you. Younger investors with a longer time horizon may opt for a higher percentage in growth investments (e.g., 80/20 or even 90/10), accepting more risk for potentially greater long-term returns.

Conversely, older investors closer to retirement might prefer a more conservative split (e.g., 90/10 or even 100/0), prioritizing capital preservation and income generation over aggressive growth. Regularly reviewing and adjusting your portfolio to match your evolving circumstances is crucial for long-term success.

| Investment Category | Example Assets | Risk Level | Potential Return |

|---|---|---|---|

| Conservative Investments (70%) | High-yield savings accounts, CDs, Money market accounts, Government bonds | Low | Low to Moderate |

| Growth Investments (30%) | Stocks, Real estate, Alternative investments | High | Moderate to High |

What is a 70/30 investment strategy?

A 70/30 investment strategy is a portfolio allocation approach where 70% of your investment capital is placed in growth assets and 30% in conservative assets. This is a common asset allocation model, particularly for long-term investors with a moderate risk tolerance.

The exact composition of "growth" and "conservative" assets can vary depending on individual circumstances, risk tolerance, and investment goals.

Growth assets are typically those expected to provide higher returns but also carry greater risk of loss, while conservative assets offer lower returns but greater stability and capital preservation.

What are considered growth assets in a 70/30 portfolio?

Growth assets in a 70/30 portfolio aim for capital appreciation over the long term. They typically involve higher risk but offer the potential for significant returns. The specific choices will depend on individual investor preferences and market conditions.

This content may interest you! Is investing young smart?

Is investing young smart?However, some common examples include:

- Stocks (equities): Investing in individual company stocks or through mutual funds or ETFs that track broad market indices like the S&P 500.

- Real Estate: Purchasing properties directly or through REITs (Real Estate Investment Trusts).

- Alternative Investments: These could include commodities, private equity, or hedge funds, though these options often require higher minimum investments and sophisticated knowledge.

What are considered conservative assets in a 70/30 portfolio?

Conservative assets are designed to preserve capital and provide a steady, if lower, return. They are generally less volatile than growth assets. Examples include:

- Bonds: Fixed-income securities issued by governments or corporations, offering a fixed interest payment over a specified period.

- Cash Equivalents: This category includes savings accounts, money market funds, and short-term certificates of deposit (CDs), which are very liquid and offer low risk.

- Annuities: While complex, annuities can provide a stream of income during retirement and offer some level of protection against market downturns, although there are often fees and limitations to consider.

How does a 70/30 strategy adjust with age and risk tolerance?

The 70/30 allocation is a starting point and is not universally suitable. It's crucial to adjust the percentages based on individual circumstances. Younger investors with longer time horizons can often tolerate more risk and may choose a higher percentage allocation to growth assets.

Conversely, investors closer to retirement often prefer a more conservative approach, gradually shifting towards a higher percentage of conservative assets to protect their principal and ensure income during retirement.

This adjustment is also influenced by individual risk tolerance: a more risk-averse investor might opt for a 60/40 or even a 50/50 split, while a more aggressive investor might lean towards an 80/20 allocation.

- Time Horizon: Longer time horizons allow for greater risk-taking, enabling a higher growth asset allocation.

- Risk Tolerance: Personal comfort level with market volatility significantly impacts the asset allocation.

- Financial Goals: The specific financial goals (e.g., retirement, education) can inform the degree of risk one is willing to take.

What is the 70/30 rule in finance?

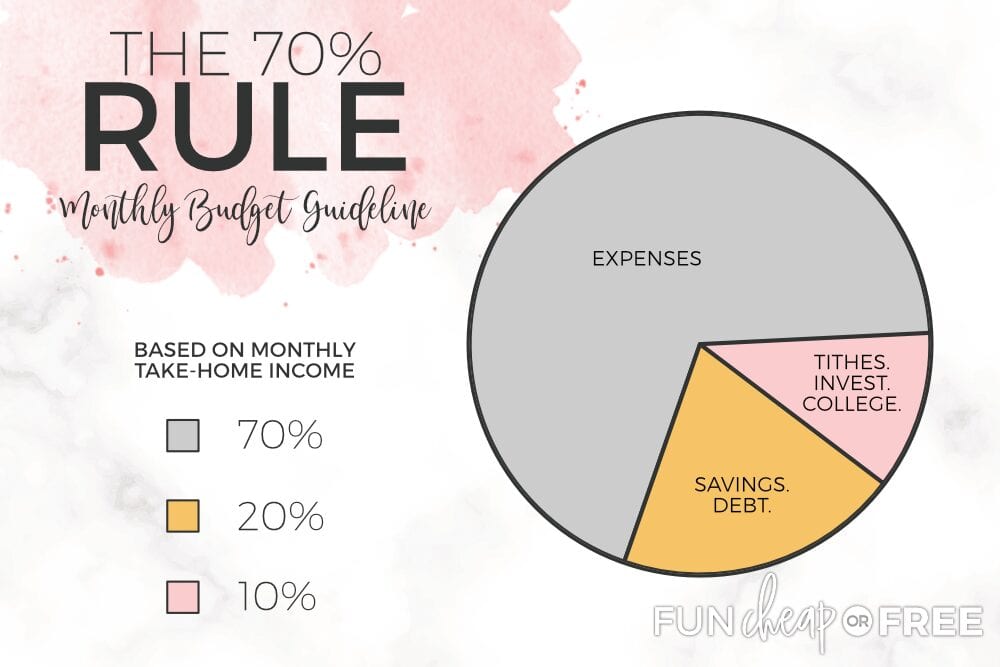

The 70/30 rule in finance is a budgeting guideline suggesting that 70% of your income should be allocated to essential expenses and savings, while the remaining 30% is for discretionary spending.

It's a simple framework designed to help individuals manage their finances effectively, prioritize needs over wants, and build a strong financial foundation. It's important to remember this is a guideline, not a rigid rule, and the specific percentages can be adjusted based on individual circumstances and financial goals.

This content may interest you! How to invest in your 50s in the UK?

How to invest in your 50s in the UK?Some people might find a 60/40 or even an 80/20 split more suitable depending on their income level, debt burden, and savings aspirations. The key is to find a ratio that promotes responsible spending habits and supports long-term financial well-being.

Understanding Essential Expenses and Savings (70%)

This larger portion of your budget covers the necessities that ensure your basic needs are met and your future is secured.

Careful planning in this area is crucial for financial stability. It's important to track spending in these categories to identify potential areas for saving.

- Housing: Rent or mortgage payments, property taxes, homeowner's insurance.

- Food: Groceries, eating out.

- Transportation: Car payments, gas, public transportation, insurance.

- Utilities: Electricity, water, gas, internet, phone.

- Debt Repayment: Minimum payments on loans, credit cards, and other debts.

- Savings: Emergency fund, retirement contributions, investment accounts.

Allocating Discretionary Spending (30%)

This smaller portion is allocated to non-essential expenses, things that are desirable but not necessary for survival.

Mindful spending in this area is crucial for preventing debt and maintaining financial control. The key is to prioritize spending based on personal values and long-term goals.

- Entertainment: Movies, concerts, dining out, hobbies.

- Clothing: New clothes, accessories.

- Travel: Vacations, weekend getaways.

- Personal Care: Haircuts, manicures, cosmetics.

- Gifts: Birthdays, holidays.

- Subscriptions: Streaming services, gym memberships.

Adjusting the 70/30 Rule for Your Circumstances

The 70/30 rule is a flexible guideline. Adapting it to your unique financial situation is key to its effectiveness. Consider factors like income level, debt, and financial goals when determining your optimal allocation. Regular review and adjustments are essential as circumstances change.

- High-Income Individuals: May allocate a larger percentage to savings and investments, potentially exceeding 70%.

- Individuals with High Debt: May allocate a larger percentage to debt repayment, reducing the amount available for discretionary spending.

- Specific Financial Goals: Saving for a down payment, a new car or education might necessitate temporary adjustments to the 70/30 ratio.

What is the 70/30 rule in trading?

The 70/30 rule in trading, also known as the 70/30 risk-reward ratio, is a risk management guideline suggesting that traders should aim to risk no more than 70% of their trading capital on any single trade, leaving 30% for subsequent trades and managing potential losses.

This content may interest you! What should a 55 year old invest in?

What should a 55 year old invest in?It emphasizes prioritizing capital preservation and sustainable growth over maximizing short-term gains. The rule isn't a rigid requirement; rather, it serves as a framework to help traders develop a disciplined approach to risk management, ensuring they don't overextend themselves on any one position.

Understanding the 70/30 Risk-Reward Ratio

The 70/30 rule dictates that for every trade, the potential profit should significantly outweigh the potential loss. This doesn't necessarily mean a 70% profit target versus a 30% stop-loss. Instead, it focuses on the proportion of your account allocated to a single trade.

For instance, a trader with a $10,000 account might risk a maximum of $700 on any one trade (7%), leaving $9300 (93%) to continue trading and absorb losses. This allows for a larger number of trading opportunities while limiting the damage from individual losing trades.

- It promotes a less aggressive trading style, reducing the likelihood of significant capital depletion from a string of losing trades.

- It encourages traders to focus on probability and consistent small gains rather than chasing large, unpredictable wins.

- It provides a framework for calculating position size, aligning with an overall risk tolerance level.

Implementing the 70/30 Rule in Practice

Implementing the 70/30 rule involves careful planning and discipline. It requires traders to define their risk tolerance level, determine appropriate stop-loss orders, and calculate their position sizes accordingly. This often involves using trading tools and strategies to accurately assess potential risks and rewards.

The rule is particularly relevant for traders utilizing leverage, as leveraged positions magnify both profits and losses, making risk management even more crucial.

- Start by determining your maximum risk tolerance for any single trade.

- Use this percentage to calculate your maximum loss in monetary terms for each trade based on your account balance.

- Set appropriate stop-loss orders to limit potential losses to the predetermined amount.

Adapting the 70/30 Rule to Your Trading Style

While the 70/30 rule offers a useful guideline, it's important to remember that it's not a universally applicable formula. Traders should adapt the rule to suit their individual risk appetite, trading strategy, and market conditions.

Some traders might find a more conservative approach suitable, perhaps a 90/10 or even 95/5 split, while others might adopt a slightly more aggressive approach, though always within carefully calculated limits.

The key is to find a risk management framework that aligns with your overall trading goals and tolerance for risk.

This content may interest you! How much should a 50 year old have in savings UK?

How much should a 50 year old have in savings UK?- Consider your experience level and your comfort level with risk.

- Adjust the percentage based on your trading strategy and the volatility of the assets you trade.

- Regularly review and adjust your risk management approach as needed.

How to calculate 70/30 rule?

The 70/30 rule, also known as the 70/30 budget rule, is a simple budgeting guideline that suggests allocating 70% of your after-tax income to needs and 30% to wants and savings. It's a flexible framework, not a rigid formula, allowing for adjustments based on individual circumstances and financial goals.

The percentages are guidelines, and the exact split might differ depending on your income level, financial priorities, and lifestyle. The key is to consciously divide your income into these two categories to gain better control over your spending habits.

The beauty of this rule is its simplicity and practicality in helping manage finances more effectively. This rule can be equally applied to business budgeting or personal finances.

- Needs: Essential expenses like housing, groceries, transportation, utilities, debt payments (minimums), and healthcare.

- Wants: Non-essential expenses like entertainment, dining out, shopping for non-essential items, subscriptions, and hobbies.

- Savings: Money set aside for emergencies, future investments, retirement, or large purchases.

Calculating Your 70/30 Budget

Calculating your 70/30 budget involves a few simple steps. First, determine your net (after-tax) monthly income. Then, multiply this income by 0.70 to find the amount allocated for needs. Next, multiply your net income by 0.30 to determine the amount for wants and savings.

Remember that the 30% portion should be further divided between wants and savings according to your individual priorities. It's recommended to prioritize saving a significant portion of this 30%, ideally aiming for a substantial emergency fund before allocating more to wants.

You can track your spending using budgeting apps or spreadsheets to monitor your progress and make adjustments as needed. Regular review and recalibration of your budget is essential to ensure it aligns with your evolving financial situation and goals.

- Determine your net monthly income after taxes and other deductions.

- Multiply your net income by 0.70 (70%) to calculate your needs budget.

- Multiply your net income by 0.30 (30%) to calculate your wants and savings budget. Allocate a portion to savings, and the rest to wants.

Adjusting the 70/30 Rule for Your Circumstances

While the 70/30 rule provides a helpful starting point, it's crucial to understand that it's adaptable to individual circumstances. High-income earners might allocate a larger percentage to savings, while those with lower incomes might need to adjust the allocation to prioritize essential needs.

This content may interest you! What is the 60 saving rule?

What is the 60 saving rule?The key is to find a balance that allows you to meet your financial obligations while still saving for the future. Factors like significant debt payments, unexpected expenses, and specific financial goals (like buying a house or paying for education) might necessitate a customized approach.

Regularly reassess your budget to account for changes in income, expenses, or financial priorities. Flexibility is key to making this rule work effectively for you long-term.

- Consider your income level: Higher income allows for a larger savings portion within the 30%.

- Factor in debt payments: High debt might require a temporary adjustment, prioritizing debt reduction before increasing savings.

- Adjust for financial goals: Saving for a down payment or education might necessitate temporarily reducing wants to increase savings.

Frequently Asked Questions

What is the 70/30 rule in investing?

The 70/30 rule is a basic investment guideline suggesting that 70% of your investment portfolio should be allocated to lower-risk, more stable investments, while 30% is allocated to higher-risk, higher-growth investments.

The 70% portion typically includes assets like bonds, index funds, or real estate investment trusts (REITs), offering relative stability and capital preservation.

The remaining 30% is designed for potentially higher returns, though it carries more volatility. This rule isn't rigid; it's a starting point, customizable based on individual risk tolerance, time horizon, and financial goals.

What are some examples of 70% and 30% investments?

The 70% (conservative) portion might include government bonds, blue-chip stock index funds (like the S&P 500), and perhaps some stable dividend-paying stocks.

These investments aim for consistent, albeit more moderate, returns over time. The 30% (growth) portion could encompass individual stocks in emerging sectors, growth stocks, small-cap funds, or even alternative investments like cryptocurrency (though this is generally considered very high risk).

The specific assets within each category will depend on the investor's risk profile and investment goals. It's crucial to diversify within each allocation to mitigate risk.

This content may interest you! How do I invest with very little money?

How do I invest with very little money?Is the 70/30 rule suitable for everyone?

No, the 70/30 rule isn't a one-size-fits-all solution. Its suitability depends heavily on individual circumstances such as age, risk tolerance, financial goals, and time horizon.

Younger investors with a longer time horizon may comfortably allocate a larger percentage to the growth portion (e.g., 80/20 or even 90/10), while those closer to retirement might prefer a more conservative approach (e.g., 90/10 or even 100% in lower-risk investments).

It's essential to consult a financial advisor to determine the optimal asset allocation for your specific needs.

How can I adjust the 70/30 rule for my personal situation?

Personalization involves considering your risk tolerance, investment timeline, and financial goals. A higher risk tolerance and longer time horizon justify a larger allocation to the growth portion.

Conversely, lower risk tolerance and shorter time horizons necessitate a more conservative approach with a larger percentage in the stable, lower-risk investments. Factors like income, existing debt, and emergency fund size should also be evaluated.

Consider seeking professional advice from a financial advisor to create a personalized investment strategy tailored to your unique circumstances.

Leave a Reply